The global central bank balancing act.

The global central bank balancing act.

Published on 6 November 2023

PERSPECTIVE

Volatility is the only certainty in FX. Just one week ago we were heading into what were expected to be the most uneventful set of central bank interest rate decision meetings in recent times. What transpired were three ‘holds’ from the BoJ, FED and BoE as expected, which one would think would surely lead to a fairly mundane week of trading? The major market-moving piece of news this week was not the central bank press conferences, but the US Non-Farm Payrolls report for October. What we saw was a modest uptick of 0.1% in unemployment and 30 thousand fewer jobs added to the economy than expected. Average hourly earnings did still increase month on month. These seem like benign numbers, but they are nevertheless regarded as the cause of a 1.5% reversal in USD. If you take a step back and look at the fundamentals of the US economy compared to that of the UK or Eurozone, the data is still extremely strong. This shows two things, firstly how important labour data is considered by traders when they are on the lookout for slack in the economy that would let central banks cut rates and, secondly, the unpredictability of FX markets. Time will tell if this is a minor correction to continued dollar strength or a reversal. But there is one thing you can say for sure without waiting: volatility is the only certainty in currency markets.

US DOLLAR

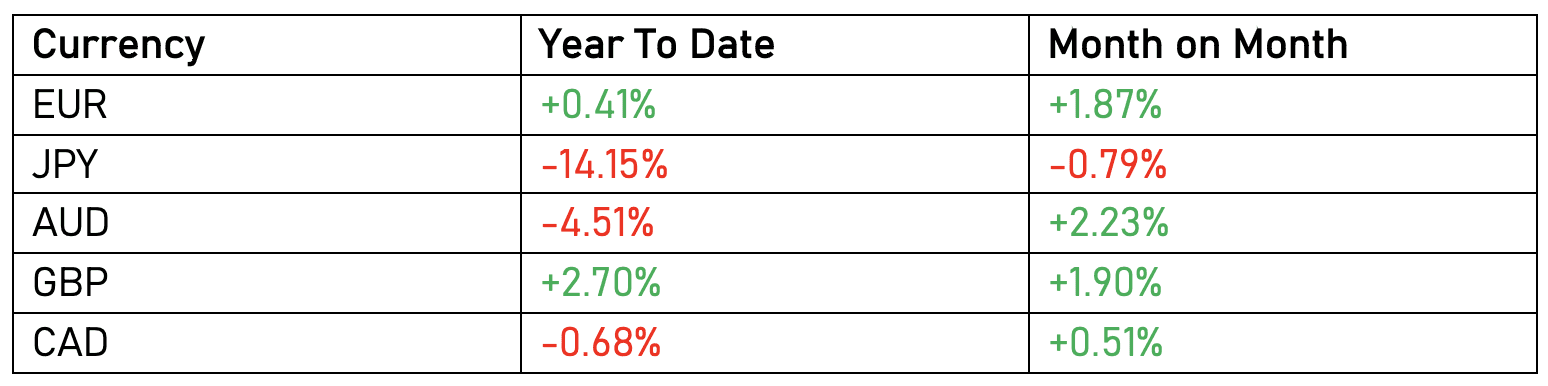

The past week we saw the US Dollar Index depreciate by 1.5% against a trade weighted basket of its peers. In a week when we expected the FED interest rate decision meeting to dominate headlines, we saw the labour market become the main driver in USD volatility, with outsized reactions to relatively small moves in jobs data.

On Wednesday the FED elected to hold rates at a 22 year high of 5.5%, as expected. Markets were more focused on what FED Chair Powell’s comments were going to be following the decision. After Powell acknowledged that economic activity, growth and employment remained extremely robust, he proceeded to state the FED would move “carefully” in their forthcoming decision making on interest rates.

There are clearly enough signs for the FED that past interest rate hikes are beginning to show their effects on the economy. Corporate and consumer debt are rising quickly and this, added to the elevated cost of borrowing, is eroding cash positions. The government itself is facing a spiraling debt issue that it must face in the year ahead, all leading to markets betting the FED is finished with its current hiking cycle. Off the back of this, the dollar is softening against its peers.

As noted, however, this was not the major market moving story of the week. Friday’s monthly non-farm payrolls report caused the largest selloff in the dollar since early July. Unemployment unexpectedly ticked up fractionally to 3.9% and 30,000 fewer jobs were added to the economy than predicted, which is not a large deviation for a labour force the size of the US. A significant weakening in the dollar ensued, with the DXY ending the week trading below 105, having hit 107 on Wednesday. The best interpretation of this outsize reaction is that markets see the payrolls data as evidence that the labour market may be turning and this, in the context of wider debt concerns, was taken as a signal that the FED hiking cycle is over too.

The fundamentals of the US economy remain exceptionally strong at this stage, but incipient signs of slowing may cause a correction in the dollar going forward. The effects of the past 18 months’ record pace hikes will start to show their full effects on the overall economy, particularly as personal savings accumulated during Covid start to run low. Markets will be keeping a keen eye on any further signs of a slowdown in the remainder of Q4.

Looking further ahead, futures and bond markets are pricing interest rates to remain at or about their current level for several years – and for as long as a decade by some estimates. While it is true that increasing trade barriers have likely created a long-run environment that is fundamentally more prone to inflation and higher rates, this is unlikely to dictate risk-free interest rates as high as 5%, and it is anyway likely to be swamped by cyclical factors in the medium term. Demand has been artificially cushioned by Covid-era savings that are not yet fully exhausted. When this cushion disappears, and effects of higher rates on mortgages, house prices, business defaults and economic activity fully bite, it is more likely that the higher rates period we are living through will prove to be self-terminating in the medium term.

Considering significant risks over this time scale, candidate Trump’s economic advisors have advanced some alarming trade policies, including a minimum 10% tariff, matching of highest tariffs, and a tariff rate that continues escalating until the US trade deficit is eliminated. This misidentifies the main cause of the trade deficit (it is driven mainly by low propensity to save and high propensity to consume in the US) and it threatens large dislocations to economies and currency markets if it comes to pass. Even a prolonged political and/or legal battle over imposing such tariffs would be disruptive to markets.

ASIA-PACIFIC

In China we saw the exchange rate post its first gain against USD since early September, ending the week trading 0.4% stronger at 7.26. Data from China last week was largely disappointing with manufacturing activity unexpectedly contracting in October. The move higher in the Renminbi was largely caused by dollar weakness following the weak labour report, rather than any positive signs from the world’s second largest economy. Data releases continue to be sparse from China so markets will be looking for signs of more economic stimulus before the path of the currency is determined. This week we have trade data and an inflation print, which will provide good insight into economic activity.

Experts on the Chinese economy have pointed out that the country has a legal system which makes it exceptionally difficult for companies to be declared bankrupt. There are similarly barriers to recognising bad debts on the balance sheets of the banking system. These both have the effect of suppressing bad news and create the risk of the financial system entering a ‘zombie bank’ state like Japan in the early 2000s, where issues cannot be resolved because they have not been recognized. More immediately, they create the risk of a major correction if the scale of financial sector issues becomes undeniable.

The Yen remained steady against the dollar last week a touch below 150. The major news following the BoJ’s decision to hold rates at -0.1% was the announcement of the unwinding of its 7-year yield curve control policy. The BoJ will be relieved at the muted reaction in yields following this announcement as it considers its next move. The obvious next step is to alter its benchmark negative interest rate to help tighten and normalize monetary policy further. This would also be seen as a positive sign for its ailing currency. The BoJ has said it is ready to intervene in currency markets if necessary but whether this takes the form of new policy instruments or a simple FX intervention is yet to be seen. Last time JPY hit 150 against the dollar it strengthened considerably on expectations of an intervention; time will tell if we see a repeat.

The Aussie appreciated vs the dollar by over 2.75% in a much-needed rebound for the struggling currency. Trading back above 0.65 for the first time since August, the currency was supported by hotter than expected retail sales and the weak labour report from the US. Other data from last week, however, was largely disappointing with house prices, exports, and commodity prices all falling short of expectations. Reports of further potential stimulus in China provides hope for some improved sentiment for the Australian economy, which relies on China to buy its vast commodity reserves. This week will be crucial for the Aussie as markets have currently priced in a 0.25% rate rise from the RBA on Tuesday. If this is exceeded, further AUD strength can likely be expected.

SOUTH ASIA

INR remained steady slightly weaker than 83 vs USD last week as the Indian economy appears to be in good health. Manufacturing and services PMIs both missed expectations but are still showing strong expansion. India is performing exceptionally well amongst large economies.

PKR depreciated by just under 1.5% against USD last week, ending the week trading at 284.5. The central bank’s decision to hold rates steady at 22% on Tuesday was backed up by a weaker than expected inflation print the following day. Consumer confidence came in better than expected but is still very low. Markets will be hoping for improved economic activity moving forward.

MIDDLE EAST AND AFRICA

The Nigerian Naira recorded one of its most volatile weeks on record with a 20% swing up and down against the dollar in consecutive days on Wednesday and Thursday. NGN ended the week trading at 767 against USD on official markets and 950 in the unofficial market. Reports earlier in the week of huge dollar demand in forex markets caused a large selloff, this was then pared by reports of a $10bn injection from the central bank. This has provided some respite for NGN (for now) and cleared a large chunk of forex demand. Whether this can be sustained moving forward is yet to be seen.

An upwards surprise to inflation in Kenya did little to arrest the slide of its currency. Indeed, central bank governor Kamau Tugge was quoted as saying the Shilling has been overvalued for “several years”. Kenya has placed restrictions on dollar buying as it is grappling with severe shortages and is struggling to meet its import demands. Further steady decline seems to be the likely path in the medium-term future.

The Tanzanian Shilling endured its most volatile week since September as Tuesday’s 7% depreciation was pared on Wednesday by news that dollar inflows from foreign direct investment, tourism, and agricultural exports matched demand from importers. The Shilling ended the week trading back at 2500 against USD.

South African Rand appreciated by over 3% against the dollar to end the week trading at 18.3. The major data release of the week showed improved import/export figures leading to a positive balance of trade and cementing itself as one of the major gainers of the week in the G20.

EUROPE

Heading into rate decision week from the BoE, there were few forecasts for GBP to appreciate against the dollar. After a turbulent week, however, sterling posted its biggest weekly gain, of over 2%, against USD following the US labour report on Friday. The BoE opted to hold rates at 5.25% in line with expectations. Other than that, there was very little to report out of the UK last week. It still has one of the highest inflation rates in the G20 and futures markets have priced in a greater chance of a hike than the FED in the coming meetings. The big fear for the UK is the worsening growth picture, with the BoE monetary policy report raising its expectations of a recession. The question is how important is price stability in the face of a negative growth outlook?

The Euro is back trading above 1.07 against USD, despite a worsening outlook in the trading bloc. The Eurozone posted negative growth once again in Q3 and this teamed with an inflation miss and further contraction in services doesn’t paint a pretty picture for the European economy. These data misses suggest the dollar was overbought prior to the FED meeting rather than a reversal in European economic activity. With headline inflation at just 2.9% and year on year and growth in negative territory, the recent hiking cycle from the ECB looks set to be complete. To appreciate from 1.07 vs USD we would likely have to see a big downturn in data from the US in the coming months. A tough time lies ahead for the European economy.

OTHER NEWS

Zambia’s central bank raised the ratio of deposits that commercial lenders must hold in a bid to reverse a slide in the world’s worst-performing currency after Argentina’s peso. The Bank of Zambia will increase the statutory reserve ratio requirement for local- and foreign-currency deposits by 3 percentage points to 14.5% with effect from November 13th.

Fitch Ratings has downgraded Ethiopia even further into junk status over concerns of a default, the agency said. Ethiopia was downgraded to 'CC' from 'CCC-', saying this reflects its view that the decline in external liquidity and significant external financing gaps have increased the likelihood of a default by East African nation. Ethiopia’s threats that it may seize a chunk of Eritrean territory in order to secure a port on the Red Sea cannot have helped its outlook in the short to medium term.

PERFORMANCES AGAINST US DOLLAR

Information as of 2023 November 6th 11.00 UAE time.

THE WEEK AHEAD

Monday, Nov 6th

EU HCOB Composite PMI

US S&P/CIPS Global Construction PMI

Tuesday, Nov 7th

Japan Household Spending

China Balance of Trade

RBA Interest Rate Decision

UK Halifax House Price Index

EU PPI

US Balance of Trade

Wednesday, Nov 8th

EU Retail Sales

Thursday, Nov 9th

China Inflation Rate

Friday, Nov 10th

UK GDP Growth Rate

UK Industrial Production

UK Manufacturing Production

US Michigan Consumer Sentiment

New to Hubpay?

We help companies all around the globe to make Corporate FX possible in the easiest and cheapest way